These are the four things you need to understand on Australian investment

While many commentators are pointing to widening credit spreads in corporate debt markets, or the hope that oil prices will lift from renewed OPEC negotiations, the following are more significant for Australian investing at present.

Michael Kloeckner, BCom LLB Dip Fin Super Director Private Clients of Clime and Head of Clime Super.

In recent weeks, I believe there have been four key economic and political factors that are highly significant for asset market psychology and therefore the direction of markets. In this context, I am considering asset markets broadly, as equity, property and bond markets must now be considered concurrently in determining the repercussions of various statements or policies.

That is not to say that asset markets are acting in a coordinated or predictable fashion – they are not.

The recent period was also one that included an extended holiday in China and a long weekend in the US. Holidays tend to stabilize markets… It’s as if frenetic trading is periodically overtaken by rational thought.

While many commentators are pointing to widening credit spreads in corporate debt markets, or the hope that oil prices will lift from renewed OPEC negotiations, the following are more significant for Australian investing at present.

The four factors that caught my eye are these:

- Japan slipped into negative economic growth in the December quarter;

- The European Central Bank flagged that it will stimulate further as deflationary pressures increase;

- The Australian taxation debate has drifted once again into a fog of uncertainty; and

- Australia’s population passed 24 million.

- Let’s consider each and develop a view on what they might mean for markets.

Japan’s lack of growth

According to the latest preliminary reading, Japan’s GDP shrank by an annual rate of 1.4 per cent during the last three months of 2015, when most economists thought it would have grown by 0.1 . That moved Japan to a full-year growth rate of just 0.4 per cent for all of 2015, which was thankfully better than 2014’s year of zero growth.

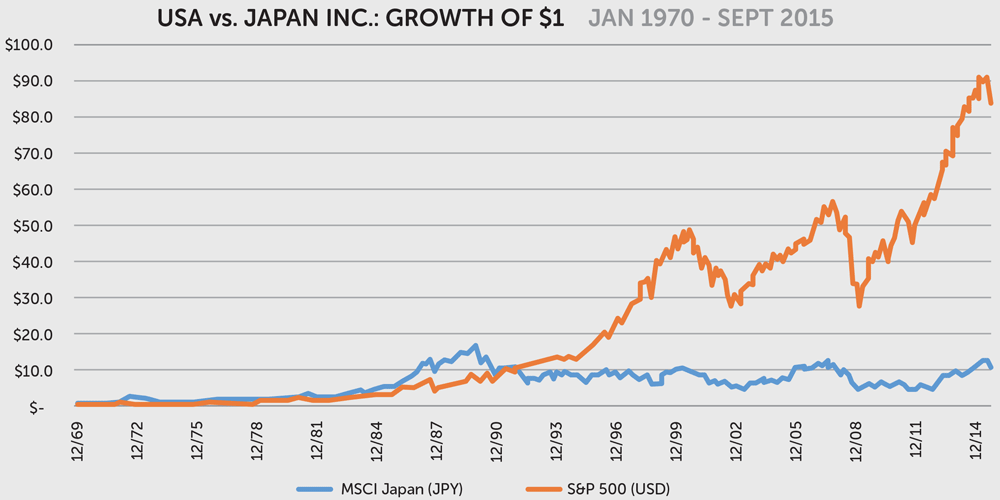

An investor in the US economy through the S&P 500 has done far better than Japanese investors in the Nikkei Index. The outperformance has been about 800 per cent over the last 25 years. No amount of monetary stimulation made a difference and maybe there is an important lesson from that observation

The contraction in the December quarter matched the fall marked in the June quarter last year. Private consumption, which makes up 60 per cent of Japan’s GDP, fell 0.8 per cent in a sign that the Bank of Japan and Government policy have so far failed to nudge households into boosting spending.

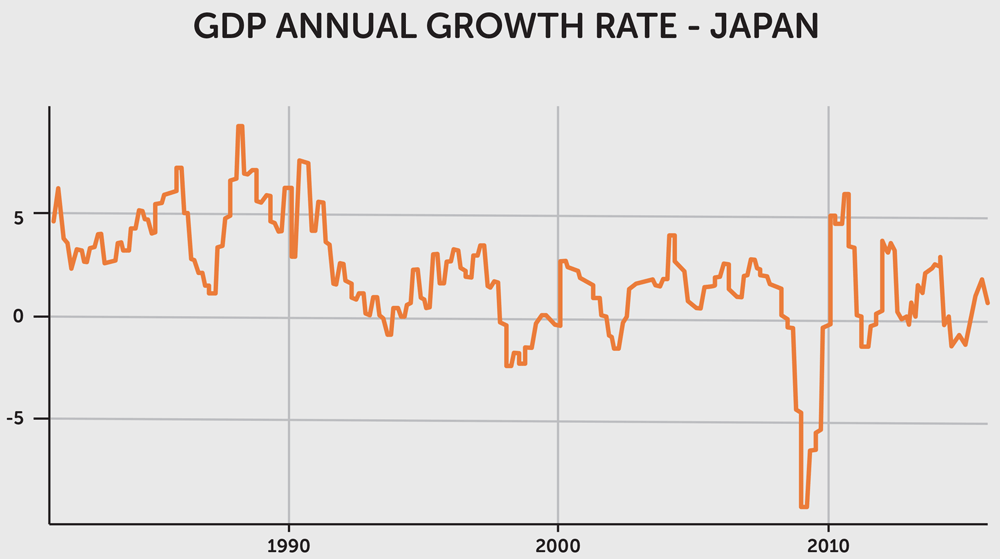

The chart (figure 1) tracks the last 40 years of Japanese GDP growth. The dynamic growth period of the 1980’s has been followed by an extended period of volatile growth around a median average of just 1 per cent per annum. There are six recessionary periods noted over the last 25 years, with the most severe being in the aftermath of the global financial crisis. Should Japan slip again into recession, this would be an extraordinary one as it would correspond to a period when the Bank of Japan had moved cash rates to negative.

The significance of negative cash rates and unrelenting quantitative easing or government money printing cannot be overstated. These policies are simply not working to bring Japan back to sustainable growth. The ageing demographics and huge public debt are weighing down the chances of recovery. Indeed the monetary policy settings are taking on the appearance of desperation as the Central Bank does the same thing over and over again for the same poor result.

The BOJ introduced a negative interest rate with the aim of discouraging investment in government bonds, thereby presumably boosting lending and bolstering investment in stocks. But the Central Bank has so far failed to achieve its objective because market players have become highly risk-averse. Now that long-term rates have gone below zero, investors will incur a loss if they buy 10-year government bonds and hold them until maturity.

BOJ Governor Kuroda has repeatedly said the Bank will cut interest rates further if necessary, and it is possible that the BOJ will opt for another rate reduction when its policy board meets in March, depending on prevailing stock prices and foreign exchange rates.

But the next chart (figure 2) shows that unrelenting stimulation has done nothing to create wealth as measured through the stock market for Japanese investors.

An investor in the US economy through the S&P 500 has done far better than Japanese investors in the Nikkei Index. The outperformance has been about 800 per cent over the last 25 years. No amount of monetary stimulation made a difference and maybe there is an important lesson from that observation.

Negative interest rates could again stir Japanese asset prices and a recent report showed how bizarre things have become in the “Land of the Rising Sun”. The BOJ’s QE policy has extended to the purchasing of property securities which are akin to the Reserve Bank of Australia buying Australia’s listed property trusts. This has supported a general lift in commercial property values with a commensurate fall in yields. Commercial property trades at yields of around 3 per cent, but such yields belie the fact that there is no chance that rents can rise due to inflation – as there is no inflation to speak of.

In any case, negative interest rates mean that major property funds or investors who borrow are now paid to borrow. That is, they receive interest for borrowing and this encourages them to buy more property at lower yields. How this ends is anyone’s guess, but it is hard to see that there will be a pleasant ending.

There is a flip side of this for Australia. QE and negative interest rates in Japan will lead to Japanese institutional bidding for our bonds, listed property trusts and infrastructure assets. The rally in these asset classes in the face of a worldwide blow-out in credit spreads is another example of the dislocation of global markets. For so long as the RBA does not see fit to restrict foreign capital emanating from QE-supported economies, then our currency will not correct appropriately and our current account deficit will not stabilize.

The European Central Bank will stimulate further

It is ‘ground hog day’ at the ECB, with Chairman Mario Draghi stating that the ECB will come forward with yet further stimulation for financial asset markets in Europe. The effect has been immediate with a stabilization of equity prices across Europe and the UK. German bank shares had been in free fall and the German equity market had peeled off 30 per cent of its value since November.

But what can Draghi really do that is different to what has already been done for years now? One suggestion was for the ECB to purchase the bad debts from Italian banks which, like German banks, are suffering substantial price declines. This was denied last week as the ECB realized that this would set an unhealthy precedent. One suspects that all European banks would be at the ECB’s doorstep with junk loans if the front door was left ajar.

The market’s expectation is that the ECB will again cut bank deposit or cash rates and drive them deeper into negative territory. In a precursor move, Sweden’s central bank, the Riksbank, dropped its rates further into negative territory. This followed comments from US Fed chair Janet Yellen reminding markets that negative interest rates are a tool the US Central Bank could wield, should the US economy need it. Not to be left out, the Swiss Central Bank is charging banks in a bid to jumpstart lending.

The problem with this strategy is obvious. It hasn’t worked in the past and it is unlikely to work this time. Both Europe and Japan need growth and the view that negative rates will drive activity is patently false. However, as bond yields begin to tumble there is a strange opportunity appearing for European Governments.

Once again, the cost of debt is plummeting for Governments and so they now can expand their deficits with cheap funding. If they embark on a massive infrastructure development plan across Europe, then growth could be achieved. That’s the good news; but the bad news is that the capital that funds this development through bonds will achieve a pathetic return. The assets supporting long term liabilities (such as pensions) will simply not generate a sufficient return and they will be sold down and switched to other growth assets aggressively on any sign of economic growth.

Once again, it is difficult to see how this plays out but it is difficult to envisage a pleasant ending.

Australia’s stalled tax debate

The desire to restructure Australia’s taxation base to ensure the funding of our needs for both an ageing and fast growing population seems to have been lost in recent weeks. Whatever momentum there was for business and broad community engagement in the restructuring of taxation has diminished. For instance, a discussion or review into raising the GST in the context of a total taxation overhaul will no longer be contemplated before an election later this year.

Frankly, the election may as well be held now as there appears to be no grand vision and there is certainly no hope for a bi-partisan approach to our long term financing needs.

The importance of broad taxation reform rather than piecemeal adjustments cannot be understated. However, many taxation strategies created in response to poorly thought out rules that were developed a generation ago, have now become embedded in Australian society – for instance, negative gearing and franking credits. The taxation minimisation schemes, sanctioned by law, are so widespread across the middle class of Australia that changes to them cannot be contemplated without broad consensus – the political risk is just too great. However, consensus requires strong visionary leadership, and Australia (like most of the developed world) defers to populism rather than pragmatism. Negative gearing and the GST are just two examples.

The social conundrum of negative gearing and its connection with GST is broadly as follows: negative gearing allows a taxpayer to offset excess interest costs (effectively interest above investment income) on an investment against other non-investment income (essentially PAYG earnings). It is used by investors seeking long term capital gains, most commonly in property investing. If income tax revenue for the Government is lowered by negative gearing, then taxation must be supplemented by either consumption or capital gains tax.

A budget and community problem eventuates because negative gearing affects the Government’s taxation receipts and it therefore affects the flows into consolidated revenue that funds healthcare, education, national security, aged care, social services and public infrastructure amongst other important public expenditures. If a significant part of the community arranges their affairs legitimately to minimize their tax and therefore their contribution to society, then it places excessive burdens on those who don’t. If everyone minimizes taxation, then a country’s infrastructure and services will drift into disrepair.

That’s why a proper taxation review must include a thorough investigation of the interaction of all forms of taxation on the economy as well as the funding of the Government to provide essential services and infrastructure. The current debate is dominated by vested interests seeking tax breaks, but appears silent as to how the community can fund its essential services.

It is our view that the stalling of taxation restructuring will slow economic activity and business capital investment in Australia. The debate around negative gearing, like most other taxation debates, has lurched into populism rather than a frank assessment of the fairness of negative gearing. It is not being assessed in connection with an adjustment to GST, or indeed the tax free threshold or company taxation rates. They are all connected.

24 million people

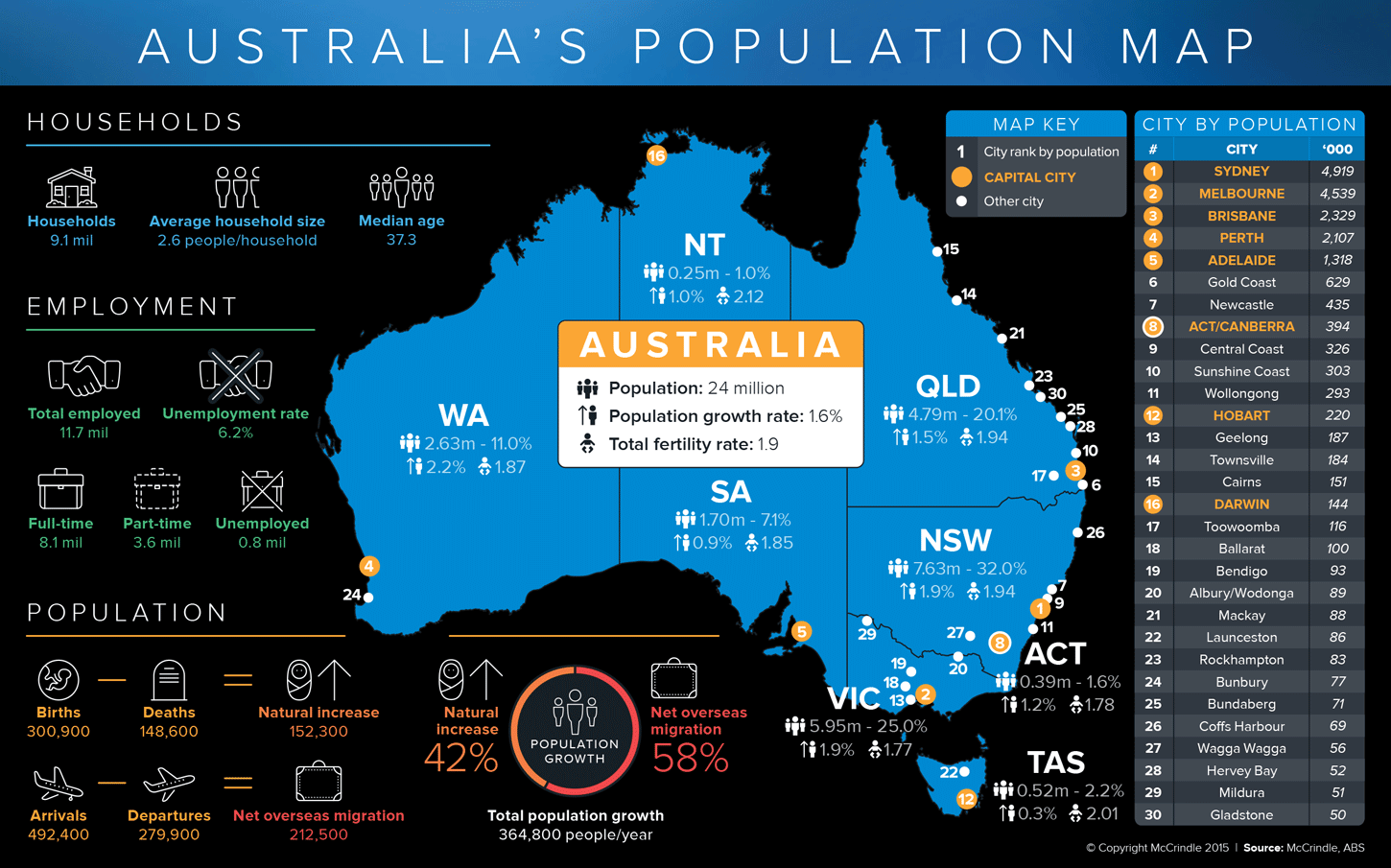

The best long term investment news this year was that Australia’s population had passed 24 million, which was well before demographers, economists and forecasters had predicted just ten years ago. It is axiomatic that the growth in population drives economic growth. While it places pressure on Government expenditure, it also enhances the opportunity for business to grow, invest and employ.

Australia is unique in the developed world. It is a democratic society with a high standard of living, national income and population growth. On a long term basis, it is hard to find a more worthy economy in which to invest. But there is and has been a massive disconnection between investment logic and outcomes. What is expected for the future is a continuation of the past, but the recent past has not been kind to the Australian equity market.

The conundrum is probably best expressed recently by the RBA’s Glenn Stevens when he stated,

“Notwithstanding below-average GDP growth, the demand for labour increased at an above average pace in 2015. The number of people employed, as measured, increased by well over 2 per cent, participation in the labour force picked up and the rate of unemployment declined, to be below 6 per cent. That is a noticeably better outcome than we expected a year ago.

This poses the obvious question of how, with apparently still somewhat below-trend GDP growth, the rate of unemployment has fallen. And whether the pattern will continue. Of course, it may be that the labour force data overstate the strength. Alternatively they may be telling us something not yet apparent in the GDP estimates. More data may shed light on this question over time.”

Australia has increased its population by 1 million people over the last 2.5 years. It has increased its population by 3 million people over the last decade. The population growth of 15 per cent in ten years has created a massive tailwind for major sectors of the economy – from retailers, builders, financial institutions, logistics and transport companies. Infrastructure owners have benefited from increased usage and toll revenue increases compounded by inflation. Arguably the recent past has presented a great operating period for Australian businesses with historic low interest rates and, more recently, a depreciating $A. Inbound tourism is growing exponentially with an influx of middle-class Chinese tourists.

However, the translation of excellent operating conditions, admittedly tempered by poor offshore economic performance, has not translated into performance on the Australian stock market. That should be a national concern and it should be part of the national debate on taxation.

Looking forward, we see continued strong population growth and supportive consumption conditions for the industries noted above. The wonder we have is whether Australian businesses, particularly at the top end of market capitalization, will continue to generate sub-optimal returns on employed capital. If they do, the equity market index will continue to trundle along in spite of the tailwinds. However, a renewed focus on economic efficiency that includes appropriate taxation structures, could propel Australia forward at a greater rate. We wait patiently for an outcome.

comments