Reasons to be cautiously optimistic

by Scott Haslem

2018 has been a challenging year for investors. After strong growth and a pick-up in inflation in the first half of 2018, growth became less synchronised and slowed as the year unfolded. This led to concerns about rising interest rates, mostly in the US which, together with the negative impact of a strong US dollar on emerging economies, threatened the longevity of the cycle. Risk events, particularly the US-China trade dispute and Brexit deliberations, also frequently dented sentiment.

These significant bouts of volatility – particularly at the start and end of the year – saw a material de-rating of risk assets, delivering more moderate returns than 2017. For the year to end November, global equities fell around 1 per cent but returned 6 per cent in Australian dollars, outperforming domestic equities which fell 3 per cent. Fixed-income returns were largely flat, as losses in credit were offset by bonds.

Looking ahead to 2019, a number of factors underpin our cautious optimism for an extension of the growth cycle – for another year at least.

A robust growth environment

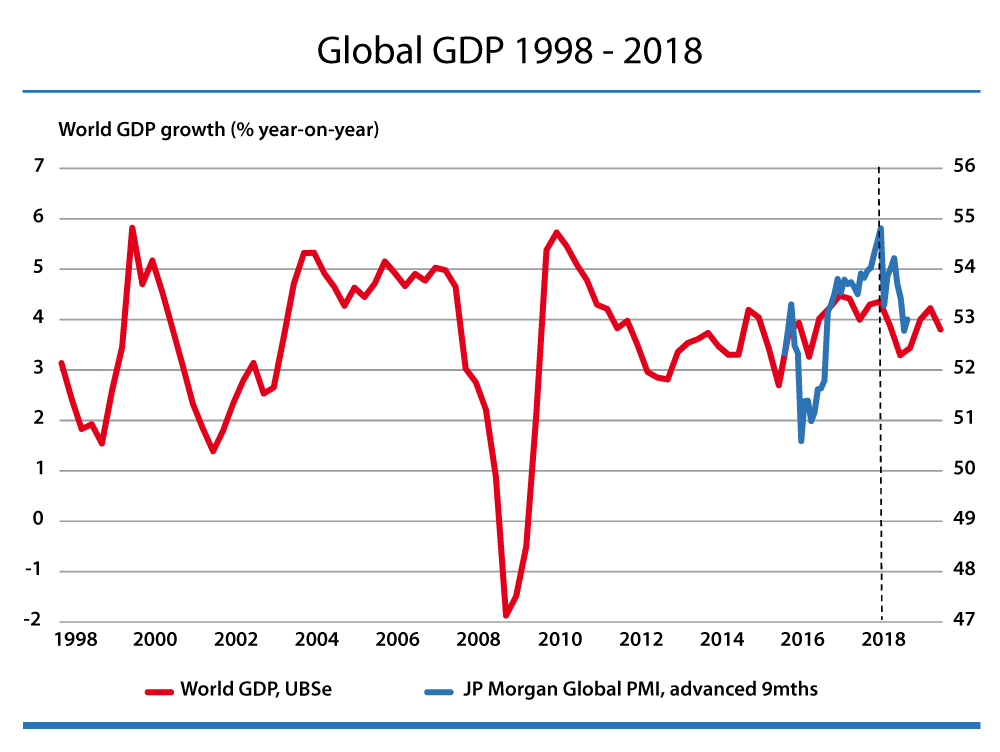

Firstly, most forecasts continue to flag a robust growth environment. Importantly, as we exit 2018, signals are scarce that a US recession – or sharp drop in global growth – is imminent.

While median global unemployment is at its lowest level since 1980, inflation (helped by the recent collapse in the oil price) looks set to rise only moderately during 2019. This reduces the risk that restrictive policy will terminate the growth cycle. Nor is there evidence of excessive credit growth or a financial crisis, key signals the cycle may end imminently. According to UBS, global growth is seen slowing from 4 per cent mid-2018 to 3.6 per cent in 2019. Similarly, in its latest November update, the OECD sees growth of 3.5 per cent in both 2019 and 2020.

Secondly, the failure of inflation to challenge central-bank targets will likely see the US Federal Reserve (the Fed) signal a less hawkish stance ahead. This could stabilise an otherwise strong US dollar and provide some relief for emerging economies. The near-solo tightening of Fed policy in 2018 should give way to more convergence in central bank rates ahead. The ECB is likely to end its bond-buying at the end of 2018 and tentatively lift rates late 2019, while moves to tighten policy in Japan and Australia will gather momentum as 2019 progresses. This is likely to underpin further rises in global bond yields (especially in Europe and Japan), weighing on credit markets.

Clouds are clearing

Finally, after a year of rapidly rising geo-political risks, we see 2019 as a year where volatility remains elevated, but the “clouds of crisis” show signs of clearing. In particular, we expect more market-friendly developments around Brexit and the EU-Italian budget dispute as we move through early 2019.

Further, following this past weekend’s G20 meeting, a material escalation in the US-China trade dispute to a third round of 25 per cent tariffs on all of China’s US-bound exports appears less likely. Together, this should allow global equities to grind higher in line with moderate 8 to 9 per cent earnings expectations (albeit Australia’s earnings are half this pace).

Key risks to our outlook centre on Fed belligerence and a third-round escalation in the US-China trade dispute.

US policy-makers may over-tighten (despite recent signs that competitive secular trends continue to moderate inflation’s rise). An unexpected jump in global inflation would deliver a similar negative impact for both equity and fixed income markets.

Another escalation in the US-China trade dispute that shunts the global growth cycle prematurely weaker and unanticipated signs of an impending US recession would be similarly problematic for equities – although in this case, defensive global bonds would outperform.

Portfolio construction is likely to stay challenging in 2019.

Sitting on the fence

We are entering the year with a neutral attitude to risk. Indeed, it is not uncommon to be sitting on the fence in regard to risk as the cycle matures. Notwithstanding our neutral equities position, we retain our recent preference for “value” relative to “growth” stocks, while also preferring global relative to domestic equities (as growth in Australia slows and political risk rises). We remain modestly overweight Europe (deep value with improving macro prospects) and emerging markets. The potential de-escalation of global trade tensions, and a less hawkish Fed that stalls the US dollar’s upward trend, are factors likely to benefit here.

For the US, perhaps one of the over-arching factors governing equity markets in 2019 will be that, for the first time in many years, cash will be a competitive, alternative asset class.

We are staying underweight fixed income, reflected most materially through credit. Global central banks will likely continue to engage in monetary-policy normalisation in 2019 and 2020, creating volatility in interest rates. The end of quantitative easing in Europe is also likely to add fuel to widening credit spreads. Domestically, the RBA is expected to remain on hold until at least late 2019. But there will be further uncertainty around how banks will be required to raise significant additional loss-absorbing capital, potentially weighing on credit markets.

Over the peak

There’s little doubt we have passed the peak in the global growth cycle. But conditions for an imminent sharp slowdown in activity are not yet in place. Growth is expected to be solid ahead, with further gradual increases in interest rates.

Amid ongoing elevated volatility – but an expectation that a number of recent risk headwinds are fading – we have upgraded equities to neutral as we enter 2019. We are also remaining particularly underweight credit markets and continue to accumulate alternative, uncorrelated assets as we transition the later stages of this cycle.

Scott Haslem is the chief investment officer at Crestone Wealth Management.

comments