Quick ways to diversify your portfolio

By ADAM SPICER

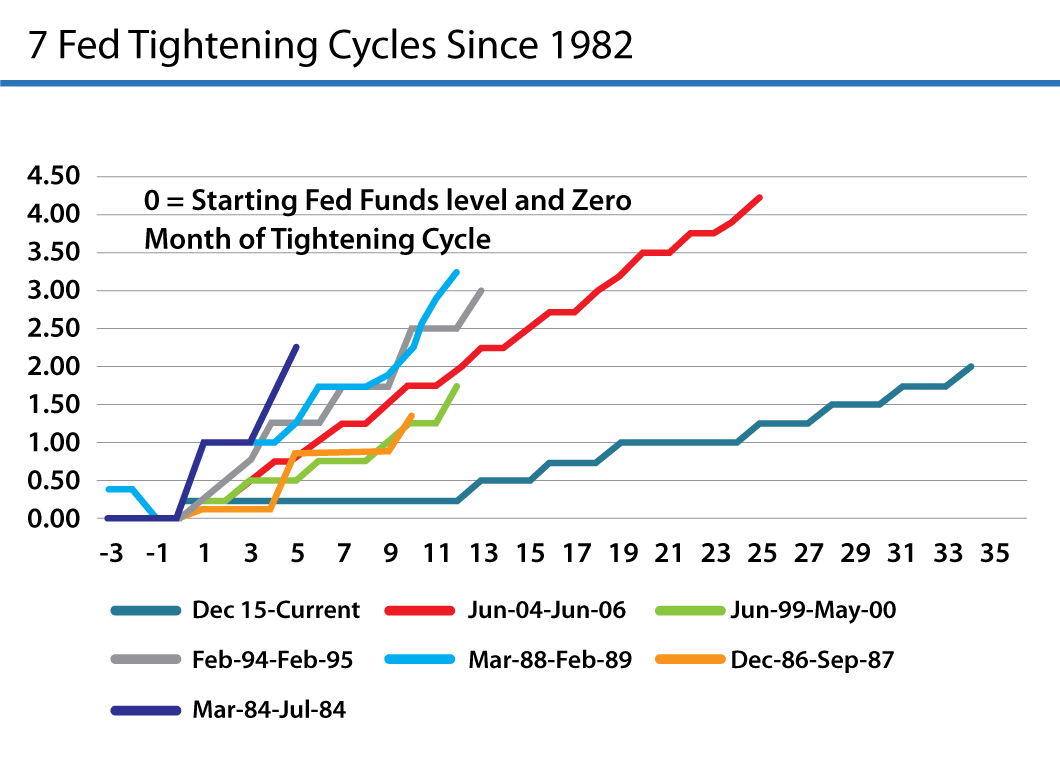

The US Federal Reserve dropped its interest rates to zero in the aftermath of the financial crisis some 10 years ago as it tried to jump-start the American economy. Then last month, the benchmark 10-year US treasury yield rose to 3.26 per cent – its highest level since 2011 – on the back of strengthening US fundamentals which is slowly lifting inflation and driving American interest rates higher.

It is therefore fair to say that we may be at an inflection point in the interest-rate cycle and, with the prospect of rising interest rates in the future, it is pertinent that investors realise the themes that drove asset returns in the past are not likely to be replicated going forward.

Investing involves trade-offs between the expected returns and the risks of meeting those returns. The majority of investors are thorough in determining which investments should form part of their respective investment portfolios. As an investor you want to make sure that any specific share or managed fund is serving a purpose and is in your portfolio because it has the potential to meet your needs and goals.

However, investors often overlook their overall asset allocation. The appropriate asset allocation and diversification is arguably the most important element investors can focus on when endeavouring to meet their long-term investment goals.

Strategic asset allocation is setting target allocations for various asset classes (including cash, fixed interest, property and shares) and rebalancing allocations periodically to ensure asset weightings are in line with investors’ risk profiles.

Research proves the key to long-term investment performance is effective asset allocation, which is responsible for 90 per cent of a diversified portfolio’s returns over time. This leaves only 10 per cent for factors such as market timing and stock selection.

Many investor portfolios include a range of direct shares and investment vehicles. Traditionally, these vehicles consisted of unlisted managed funds (MFs) and listed investment companies (LICs). However, recently there has been an onslaught of new vehicles, structures and issuances which has added diversity to the investment landscape. These investments provide investors with a great deal of choice and opportunity when constructing and blending different portfolio exposures into their asset allocations.

Exchange-traded funds (ETFs) and LICs are assets that can be bought and sold on the Australian Securities Exchange (ASX). Their popularity with investors in recent years has risen significantly. Another method many investors utilise to access these similar investments is through unlisted MFs.

LICs, ETFs and MFs defined

Whether you choose to invest through an LIC, MF or an ETF you are essentially purchasing a portfolio of individual assets (also referred to as buying a basket). You purchase units/shares in the investment and this gives you exposure to a portfolio of underlying investments.

Depending on the individual security, the underlying investments are chosen as they are a constituent in the reference index (whether this be a so-called passive market cap weighted index, or a smart-beta index which has some quantitative overlays) or they are selected by the portfolio manager for any number of reasons in an active strategy.

Let’s outline the difference between index and active.

Index: Investments that use an indexing approach seek to track a specific market or sector index. Some of the benefits of index investing are low operating costs, diversification, tax efficiency and simplicity.

The value of an index ETF/MF will move in line with the index it tracks. For example, a five per cent rise or fall in the index would result in approximately a five per cent rise or fall in an ETF/MF which tracks that index (all other things being equal).

Active: An active investment strategy doesn’t track an index but rather uses a specific investment approach/ strategy to achieve a particular outcome such as outperforming an index or minimising the impact of market volatility. The portfolio manager will select underlying constituents of the portfolio based on an “investment mandate”.

How they differ

The main difference between LICs and ETFs/MFs is that they have different structures.

LICs are companies, which means they are “closed ended” and have a fixed number of shares. Of course, they can always increase the shares on offer through a capital raising or reduce them through a buy-back but neither of these options is a simple or easy process.

Essentially, LICs trade on the market and investors buy and sell them from each other as they desire. While the market sets the price you pay for the LIC, it might not necessarily be the same as the value of the underlying investments or net tangible assets (NTA). It is a common occurrence for an LIC to trade at a premium (when the share price is higher than the NTA) or a discount (when the share price is lower than the NTA) to the NTA.

ETFs are open-ended unit trusts, which means they incur unlimited (depending on the underlying securities they own) daily in-flows and out-flows of funds. While there are a number of units already available on the sharemarket, units are also made available on the market by “market-makers”. Each ETF trading on the ASX has one or more dedicated market makers. Uniquely to ETFs, these market makers have an ability to add to or withdraw from the supply of ETF units by trading directly with the ETF issuer.

MFs are also open-ended unit trusts and incur unlimited (depending on the underlying securities they own) daily in-flows and out-flows of funds. However, they differ to ETFs as they are not traded on market. Instead, applications are made to acquire or redeem funds and the number of units you are allocated depends on how much money you invest. Each day the fund will process acquisitions and redemptions after the close of the market and create extra units or unwind units should there be a difference one way or the other.

The advantages of using ETFs, LICs and MFs

Exchange traded – ETFs and LICs are traded on the ASX so they can be bought and sold easily, with funds being available two days after the sale.

Easy diversification and reduced single stock risk – As these investments will include a number of underlying holdings, the purchase of the investment will give the investor exposure to the underlying portfolio in an efficient and cost-effective manner.

Simple administration – Some investors don’t like the administration and paperwork involved with owning individual stocks. In addition to the paperwork there are decisions to be made around corporate actions and portfolio holdings. Owning these investments enables the investor to transfer much of this burden to the manager/issuer.

Efficient way of building other exposures that may not already exist in the portfolio – It can be difficult to gain exposure to some investments (for instance international equities) and by using any of these the investor will be able to add those exposures in an easy and cost-effective manner.

Great for ‘set and forget’ portfolios – For investors who want to purchase a portfolio and leave it alone, these types of investments may be a good option as they reduce the risk of single-stock exposures.

Great for low balances and beginner investors – These types of investments provide a good way for those with low balances or beginner investors to build a portfolio. With one or two holdings, a broad diversified portfolio can be built at relatively low cost.

While it is difficult to pick which asset class will outperform in a given year, it’s prudent portfolio management for investors to focus on constructing a well-diversified multi-asset portfolio comprising different asset classes which are non-correlated. The use of ETFs and LICs has made it more efficient and cost-effective to build the correct structure and portfolio allocation, which should have the benefits of reducing portfolio volatility and assisting investors in achieving solid long-term risk-adjusted returns into the future.

Adam Spicer is a financial adviser

with Baillieu.

comments